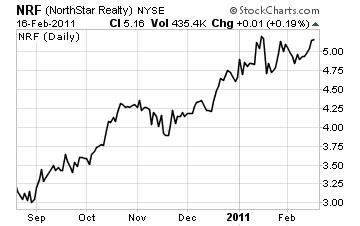

As I’m looking at this chart, all I can think is… “I know what’s happening!”

I found a stock that’s caught the eye of investors. The stock bottomed in July of 2010 and has been shooting for the moon ever since.

This stock is up almost 103% in just 7 months.

Is it too late to get on board?

Not by a long shot. Back in 2007 this stock traded for over $10 a share… If it reached the old highs, it could double in value again! And I think we’ll get back to that level in the next few months.

But that’s not the only reason why I like this company.

The stock I’m going to introduce to you is in an industry poised to rebound…They have a unique business model generating hundreds of millions in revenue… the stock is hugely undervalued… and the stock pays a fat juicy dividend.

Do you really need more of a reason to buy?

I didn’t think so… now without further delay let me introduce my latest hot stock pick.

COMPANY DESCRIPTION

The company I want to introduce to you today is none other than NorthStar Realty Finance Corp (NRF). They trade on the New York Stock Exchange for about $5.18 a share.

The stock has seen a huge run in the last few months… but I’ll get to more on that in a moment. First, I want to tell you more about what this company does.

NorthStar first and foremost is a REIT.

In other words, they are a Real Estate Investment Trust (REIT). That means two things… first, they are focused entirely on the real estate industry. And second, as a REIT they are required by law to pay out a big portion of their profits to investors.

So what do they do?

It’s a bit complicated, but in a nutshell, NorthStar uses their capital… their cash… to buy real estate securities. They leverage up the investment and use cheap money to buy mortgage backed securities, rated notes, mezzanine financing, structured financing, secured financing, and other real estate debt.

These investments throw off nice streams of cash…

Best of all, the cash profits get returned to shareholders – just like you and me!

NORTHSTAR’S BUSINESS

Now, you know NorthStar invests in real estate securities… but that’s not all they do.

NorthStar sets itself apart from the pack by also taking its business a slightly different direction. They offer what they call “Net Lease Properties.”

This is a very unique strategy.

The company partners with a corporate client who needs to operate in a big space.

NorthStar invests in the property and signs a net lease with the tenant. They only do this with big organizations.

It’s a great deal for both parties.

The corporate client gets a great piece of property without having to front all the cash to buy it. NorthStar grabs a nice piece of real estate and now has a solid tenant who signs a long term lease and pays all the bills. The arrangement is designed to throw off a nice stream of profits too!

Now, I know what you’re thinking… real estate!?!

The entire industry has been in the trash lately. The homebuilders are getting crushed.

Home values are down across the board. And the news is filled with horrible stories about rampant foreclosures. The commercial market isn’t any better!

Despite the horrible news, the industry isn’t going away.

Think about it. We’re always going to need a place to live and an office to work in. We’re going to need manufacturing plants, and production facilities… and distribution centers.

The heart of all these locations is real estate… and despite the recent market turmoil, now’s the time to be buying.

You buy when prices are low.

You buy when other investors are afraid.

You buy when nobody else is… and that’s when you grab the really big profits.

And that’s what NorthStar is doing. They’re holding tight to the real estate market.

They’re using this challenging time to buy up good quality securities and properties nobody else wants.

Here’s a perfect example…

Just a few months ago, NorthStar bought $28 million worth of real estate notes for only $2 million. Does that mean they just made $26 million? Of course not… but if these notes return just 20% of their original value, NorthStar (and their shareholders) will be making big money!

Clearly, the financial situation is key – so let’s take a closer look.

NORTHSTAR’S FINANCIALS

Now the third quarter was a bit rough…

Revenue was strong at over $126 million. Most of this was interest income from their portfolio and rent payments. However, the company did post a loss. Net loss to

common stockholders for the third quarter 2010 was $144.1 million. That’s about $1.87 per share.

However, keep in mind, $198 million was due to an unrealized loss on their investments. If you kicked just those losses out of the numbers, the company would have been profitable.

Now, before you start worrying, remember – we’ve just survived one of the most brutal economic recessions of our time. As we see the markets improve, I believe the company will see its portfolio increase in value again… not fall. And that will provide a huge driver to the stock.

Now the valuation on this company is a little ridiculous.

I feel like I’m buying the Tiffany Diamond for $5.18 at a garage sale!

Consider their book value. That’s the value of all the assets after subtracting out all of their debts. The book value is $15.78 per share! Right now you can buy the stock for a 60% discount off of book value… that’s a huge deal.

Another valuation metric I like to look at is Dividend Yield.

As a comparison, the S&P 500 dividend yield sits at around 1.78% right now. So, for every $100 invested, you get back $1.78.

With NRF it’s a little different.

NRF paid out a dividend of $0.10 last quarter (and have for the last 8 quarters). Assuming they continue paying out at that rate… it means the company is sending about $0.40 a year to shareholders.

With a stock price of just $5.18, it works out to a dividend yield of about 7.75%.

In a nutshell, for NRF to reach parity with the S&P 500 on a dividend yield basis, the stock would have to climb by over 440%!

If that’s not a nice return I don’t know what is!

Now, I’m not the only one who likes this company. While doing my research, I came across a document filed with the Securities & Exchange Commission. It’s form SC- 13G/A, filed by none other than the investment company BlackRock.

In case you didn’t know, BlackRock is one of the largest investment managers in the world.

They manage more than $3.56 trillion dollars of capital.

Here’s the takeaway… According to these filings from early February, BlackRock owns over 4 million shares of NRF in their various funds. That’s more than 6.35% of the company.

Clearly they see the huge upside potential like I do!

ANALYSIS OF NRF STOCK

The stock is volatile and tends to bounce around a lot… but that’s “OK.” This is one company you want to buy now and hold for a while. Given the improving industry fundamentals, low book value, high dividend yields, and great market position… this stock could be a huge winner for us.

Chart courtesy of StockCharts.com

ACTION TO TAKE

If you like what you’ve read, do your own research… then Buy NRF up to $5.35 a share.